If you go to the United States to go public, what other stories can Luckin tell?

Luckin, which was once mired in financial fraud turmoil and was forced to retreat to the pink sheet market, is now going to return to the U.S. stock market with nearly 30,000 stores.

This news comes from Luckin co-founder and CEO Guo Jinyi. He admitted at the recent Xiamen Entrepreneur Day conference that the company is actively promoting a return to the US main board. The subsequent release of the third quarter results also added a fire to this ambition in a timely manner.

There are many eye-catching figures in the financial report: the total revenue in the third quarter was 15.287 billion yuan, a year-on-year increase of more than 50%; The average number of monthly transaction customers exceeded 112 million, a record, and same-store sales of self-operated stores increased by 14.4%, and cooperative stores also performed vigorously - revenue was close to 3.8 billion yuan, an increase of 62.3%.

Growth is always the favorite story of capital. Therefore, putting aside the stricter process and compliance issues caused by financial fraud, Luckin still has to face a core question: how long can such growth last?

This requires considering the following questions - where is the ceiling of the number of stores? After 30,000 stores, how many dividends can continue to be encrypted? And, where is the limit of the output of a single store? As the popularity of takeaway subsides, what will Luckin do?

1. How many stores can be opened?

Luckin has set many records worthy of being recorded in business textbooks.

In terms of business model, Luckin uses "Internet thinking to make coffee", uses subsidies to cultivate user habits, and uses data to drive operations; In terms of products, Luckin has manufactured many explosive products such as raw coconut latte and sauce latte; In terms of marketing, from co-branded cross-border to social communication, Luckin is good at creating "out of the circle" events.

Then there is the myth of store opening speed.

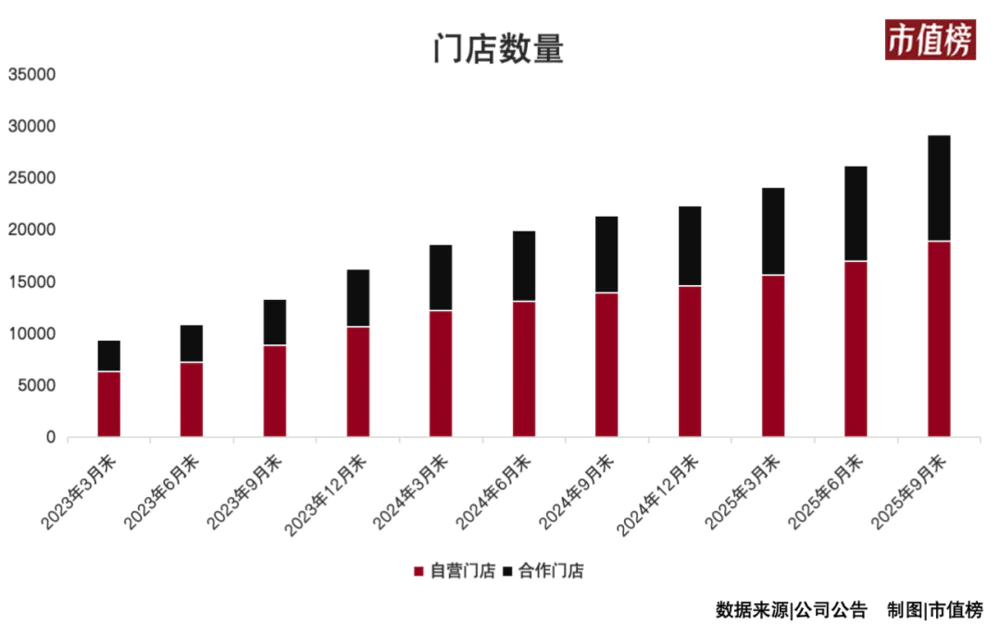

From 2023 onwards, in the process of playing with Cudi, Luckin will accelerate its expansion through the "franchise with stores" model, with more than 10,000 stores in June, more than 20,000 stores in July 2024, and 29,214 stores by the end of September 2025. In the past two years, Luckin has added one store every 1.1 hours on average.

The number of Luckin stores has left Starbucks (8,000+) far behind. So, where is the upper limit on the number of stores in Luckin?

Guo Jinyi pointed out in the conference call that China's coffee industry is still in the early stages of development and high growth, so "business growth and market share expansion remain our strategic priorities at this stage." ”

A research report by Huayuan Securities calculated based on per capita disposable income that the upper limit of Luckin's store space is 39,000 when the per capita disposable income of urban residents remains unchanged (compared to 2024), that is, there are less than 10,000 stores.

In the middle of this year, the number of stores in Mixue Bingcheng (excluding Lucky Coffee) was in the early 40,000s, and there was already pressure on single-store revenue, taking the initiative to slow down the pace of expansion.

Theoretically, judging from the two sets of data of "there is still 10,000 store opening space" and "self-operated store same-store sales increased by 14.4%", the inflection point between Luckin stores and the decline in single-store revenue seems to be far away.

However, we also noticed some bad signs.

Taking Q3 of self-operated stores as an example, same-store sales increased by 14.4%, compared with a decrease of 13.1% in the same period in 2024, so that single-store sales are similar to Q3 in 2023, and even slightly lower this year.

Let's take a look at the cooperative stores.

We take the amount of materials purchased by the cooperative store from Luckin as a reference, after all, more revenue and higher order volume need to consume more coffee beans, coconut milk, milk and other materials.

The change in the amount of materials purchased by cooperative stores from Luckin represents the change in the average number of cups sold in a single store to a certain extent.

On an average basis, the number of cooperative stores in Q2 and Q3 in 2025 increased by 29.2% and 36.7% year-on-year, and in the same period, the materials entered by cooperative stores from Luckin were 1.75 billion yuan and 2.02 billion yuan respectively, an increase of 29.2% and 22.5% year-on-year.

In other words, the average amount of materials purchased from Luckin by each cooperative store is declining, with 204,000 yuan and 231,000 yuan in Q2 and Q3 in 2024, and 197,000 yuan and 207,000 yuan respectively in the same period in 2025.

If you consider that in the second and third quarters, the takeaway war "subsidized" a large number of tea and coffee orders, this signal is even less optimistic.

As mentioned earlier, Luckin's revenue from cooperative stores was close to 3.8 billion yuan, an increase of 62.3%, while the increase in material sales was not high, and the growth points worth paying attention to were profit commissions and equipment sales.

In the second and third quarters of this year, Luckin's profit commission from cooperative stores (according to the tiered system according to the gross profit of different stores) and the increase in equipment sales far exceeded the increase in the number of stores.

The tilt of the product structure towards low-cost categories has led to an increase in gross profit margin, which can explain part of the reason. But there is also another possibility, that is, Luckin's cooperative stores have been significantly replaced.

The old cooperative stores that make money have brought higher gross profits due to takeaway subsidies, so they have distributed more profits to Luckin, and a large number of old stores that do not make money have been closed, and at the same time, a large number of new stores have opened, and more equipment needs to be purchased.

The optimistic situation is that the stores with bad traffic points are closed and stores are opened at better points, and the pessimistic situation is that the good points are almost occupied.

In fact, as early as July 2024, when there were a total of 20,000 Luckin stores, Jihai brand monitoring said that 47% of Luckin Coffee's stores were encrypted stores, and the average shortest distance between stores was only 403 meters.

This distance is shorter than Guo Jinyi's imagination many years ago that "in the core area of the city, you can see a Luckin coffee every 500 meters, and busy people can get coffee more conveniently".

Although the number of Luckin stores is still growing rapidly, and there is still nearly 10,000 store space in theory, in fact, the physical ceiling of the store network may be very close, and if it continues to open, it will face the challenge of "left hand hitting right hand".

2. The takeaway subsidy will be refunded, and the "nine yuan nine" label is difficult to get rid of

When the ceiling of the number of stores looms, Luckin faces a more essential challenge: how to reconstruct the profit model. Then I have to mention that the key factor that has recently disturbed Luckin's profits: takeaway.

In the third quarter of 2025, although Luckin's revenue increased by 50.2% year-on-year, net profit fell by 2.7% year-on-year. Among them, a key data is that distribution expenses soared by 211.4% to 2.89 billion yuan, and this huge expense accounted for 18.9% of revenue. In other words, for every 100 yuan of income, nearly 19 yuan needs to be paid to the distribution link.

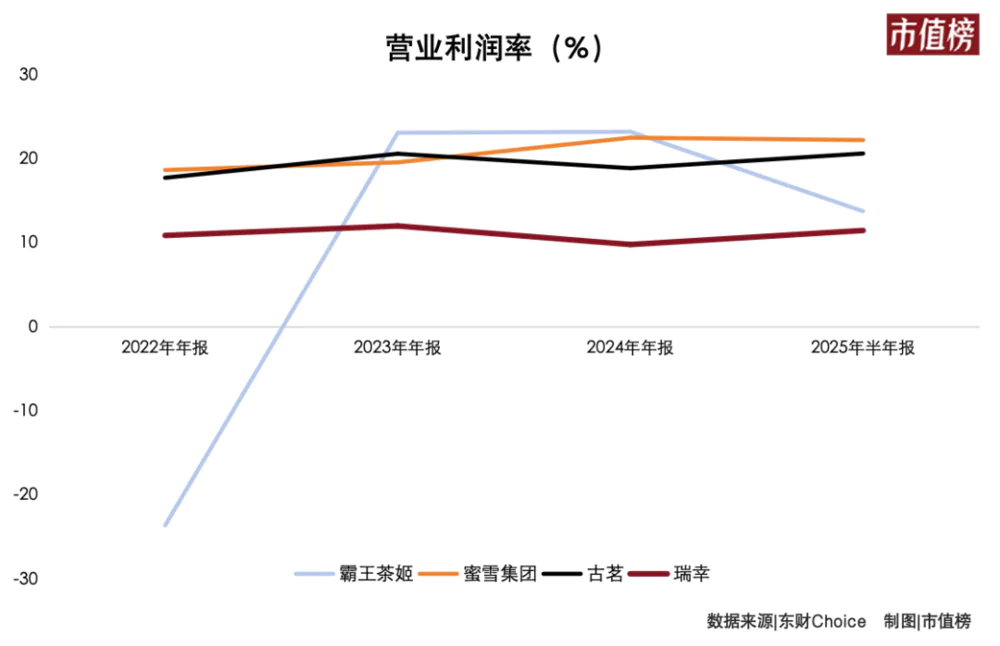

Guo Jinyi also admitted, "In the short term, the proportion of takeaway has increased significantly, which will indeed have a certain negative impact on profit margins." From the data point of view, Luckin's operating profit margins in the second and third quarters were 21.0% and 17.5%, respectively, compared with 21.5% and 23.5% in the same period in 2024.

At the same time, Guo Jinyi also said that "takeaway is only a short-term starting point" and "the long-term development of the coffee industry will still be centered on self-pickup".

So, what does it mean if Luckin successfully returns to the normality of self-pickup?

This is a complex pros and cons.

On the bright side, huge fulfillment fees will be significantly reduced, which opens a critical window for profit recovery. But challenges also follow: when the tide of takeaway traffic recedes, the number of store orders will inevitably fall. The fixed costs of the store (such as rent, equipment depreciation) will not be reduced accordingly. What Luckin needs to accurately calculate is: can the saved distribution costs cover the profit loss caused by the decline in order volume?

When the marginal benefits of increasing the number of stores decrease, when the tide of takeaway subsidies fades, Luckin's sustained growth still needs to look at pricing.

Luckin's organizational and operational capabilities are naturally worthy of recognition, but on the whole, Luckin's operating profit margin is lower than that of milk tea shops that also focus on self-pickup, Mixue Bingcheng, Gu Ming, and Bawang Chaji.

Now, Luckin has been firmly locked in the "9.9 yuan" price mentality created by himself, and the takeaway subsidy has lowered this figure.

On the surface, Luckin's co-branded gameplay emerges one after another, from Moutai, Black Myth Wukong to Line Puppy to Moutai, trying to soften consumers' price sensitivity with emotional added value.

Most of the time, these co-branded models cannot fundamentally change the value perception of the brand. The current co-branding strategy is more like a superficial "packaging creativity competition". On social platforms, consumers are keen to discuss "which co-branded packaging is better" rather than "Luckin's coffee tastes better".

Luckin co-branding is like flowing water, plus other brands can also play co-branding, such as the co-branding of Cudi and Nezha, this kind of interaction that stays at the level of visual freshness, the stimulation of consumption impulses is becoming more and more limited.

What is even more alarming is that in addition to the intensive co-branding, although the frequency of new products has not decreased and the number of stores has increased significantly, it is difficult to reproduce the phenomenal explosives of the "thick milk latte" and "raw coconut latte" levels. Innovation has degenerated from a sharp tool to establish category barriers to a conventional action to maintain market volume.

On the other hand, Luckin is no longer facing competition in the coffee industry. As Li Hui, chairman of Luckin and founder of Dazheng Capital, the largest shareholder, said in an interview, "The coffee market and the milk tea market are not absolutely divided, but blended with each other." This means that Luckin's pricing should not refer to Starbucks, but to the average price of 6~8 yuan from Mixue Bingcheng and about 15 yuan of fresh milk tea from Heytea.

3. New challenges in overseas markets

As the competition in the domestic milk tea and coffee markets becomes more and more fierce, Luckin has to look at a farther boundary - overseas markets.

At present, Luckin has opened 118 overseas stores in Southeast Asia, North America and other places. The scale of 118 is less than 0.4% compared with the volume of nearly 30,000 in China.

More importantly, overseas operations face new challenges. Compared with the concentration and unification of the Chinese market, overseas markets are highly decentralized.

Dispersion is reflected in multiple dimensions, and there are significant differences in consumer tastes, regulations and policies, supply chain infrastructure, etc. in different countries and even different regions of the same country. This means that instead of simply copying and pasting China's successful model, it requires a costly localization adaptation from scratch in each new market.

Decentralization also directly pushes up operating costs, making enterprises must reach a certain store density and business scale to cross the profit threshold.

This means that the supply chain needs to be rebuilt, consumer habits need to be cultivated, brand recognition needs to be cultivated, and localized tastes need to be explored. Guo Jinyi once described that in the world coffee market, China is a market for "picking up money" and overseas is a market for "grabbing money".

In the U.S. market, Luckin has abandoned its low-price strategy, and its product pricing focuses on the mid-range, slightly lower than Starbucks. This differentiated positioning shows Luckin's expectations for profit space in overseas markets.

The same is true in the Singapore market, for example, the signature raw coconut latte Singapore store is priced at S$8, with a discount of S$5.6 (about 31 yuan), while Starbucks Singapore is priced at S$6.0~8.7 (about 32~47 yuan). Although Luckin attracts new customers through preferential strategies such as the first cup of S$0.99, the overall price advantage is not obvious compared to Starbucks. Singapore's first Luckin store opened in 2023, but Luckin's business in Singapore has not yet achieved profitability in the first three quarters of 2024.

All in all, Luckin's overseas expansion story is still in the preface, there is a lot of room for imagination, but the path to fulfillment is unknown, and it will take a long time to verify, and Luckin needs to prove that it can successfully replicate its business model, not just serve the Chinese community.

Overseas markets may be the foreshadowing of the next round of growth, but they are not a fast-acting medicine for current growth anxiety. Luckin still needs to answer the most fundamental question on the battlefield of its main business: how to make every store make healthy money on the basis of the scale of 30,000 stores.