The real test of Ali is the upcoming "Battle of Tianwang Mountain"

In the winter of 2025, we are once again witnessing the fickle nature of the business world.

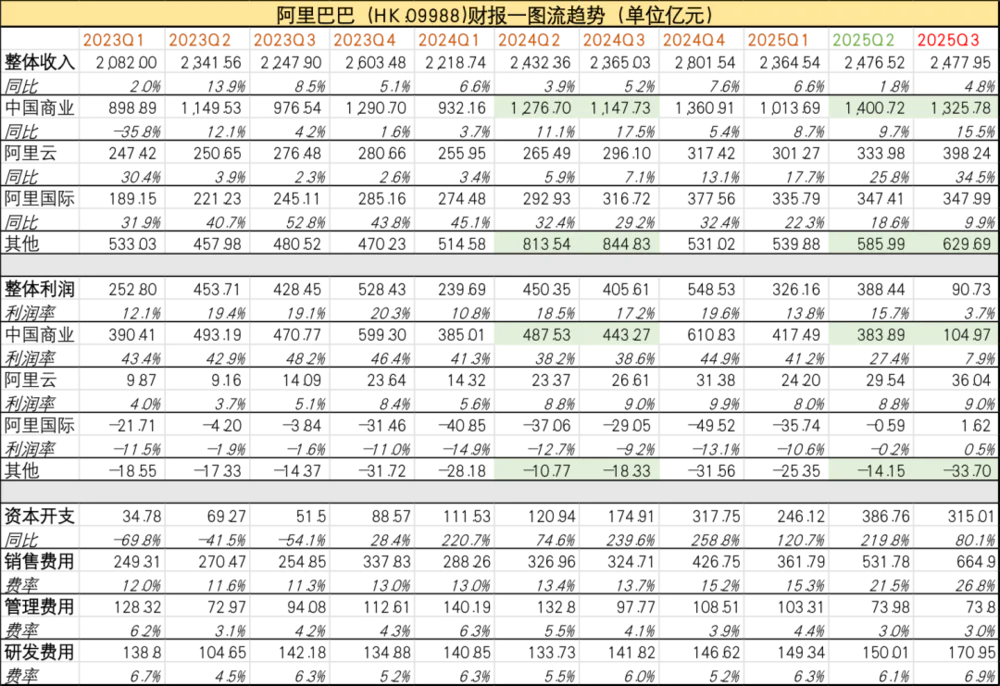

On November 25, Beijing time, Alibaba released its results for the third quarter ended September 30, 2025. According to the financial report, Alibaba's revenue reached 247.8 billion yuan, slightly higher than market expectations; adjusted EBITA was only 9.073 billion yuan, a sharp decrease of 73% year-on-year; Non-GAAP net profit was 10.352 billion yuan, down 72% year-on-year, lower than expected. The core financial data are shown in the figure below (green is the adjusted caliber, and non-synchronous periods cannot be directly compared):

Picture: Alibaba financial report summary, source: corporate financial report, compiled by Jinjin Research Institute

As the absolute focus of the current Chinese market, this financial report can be said to have whetted investors' appetites, and the release time was even delayed by an hour than usual. Overall, Alibaba still sends some positive signals on its books: revenue slightly exceeds expectations, cloud business performance is impressive, and capital expenditure continues to remain relatively high.

However, combined with the significant decline in profits in the third quarter, weak e-commerce growth, and aggressive expansion in the past few quarters, Alibaba seems to be "powerless" again - the once delicate balance is becoming increasingly difficult to maintain while maintaining both the basic e-commerce market and the commanding heights of AI.

The cracks in Alibaba's "Iron Throne" have appeared, and at the same time, what is more urgent is that the new "PLUS version" opponent is rushing: according to previous market sources, today's capital led by Xu Xin, the "queen of venture capital", bought ByteDance's old shares. According to the transaction consideration disclosed by the media, Byte's current valuation has reached US$480 billion, or about 3.4 trillion yuan. If this information is true, it means that Byte has surpassed Alibaba (Alibaba's current overall valuation is about 2.7 trillion yuan) to secure the second place in the valuation of Chinese Internet companies.

From the perspective of business layout, there is no essential difference between Byte and Alibaba: both take e-commerce as the basic market of cash cows and AI as the core goal of long-term development. In other words, what Ali can do, Byte can do.

1. E-commerce and AI are battlegrounds

The competition that Alibaba has to face today is fundamentally different from the "AT competition" (Alibaba and Tencent) ten years ago.

Looking back at Tencent after 2015, its ecological strategy of "handing over half of its life to partners" has made its competition with Alibaba more manifested as an "agent war" - JD.com, Pinduoduo invested by Tencent and Alibaba compete in the field of e-commerce, but Tencent itself does not end directly. The core businesses of both parties, social networking and e-commerce, are still maintaining a safe distance.

Today, Alibaba and Byte are a comprehensive collision of core interests.

Specific to the product line, almost all of Alibaba's core business is facing head-on competition with Byte:

(TikTok shop vs 速卖通/Lazada)

E-commerce (Douyin e-commerce vs Taotian), cloud services (Volcano Engine vs Alibaba Cloud), AI entrance (Doubao vs Qianwen), local life (Douyin vs AutoNavi), corporate services (Feishu vs DingTalk), cross-border e-commerce (TikTok shop vs AliExpress/Lazada) ……

In international relations, there is a famous "Thucydides trap" - when emerging powers challenge the conservative powers, the space for compromise is extremely compressed due to the comprehensive overlap of the core interests of both sides. Today's Byte and Alibaba are facing a similar situation.

With "e-commerce-AI" as the axis, every position is a battleground, and every step back means strategic passivity. Among the many business lines, the most important thing for both sides to lose is e-commerce and AI.

First of all, e-commerce is the foundation of Alibaba and Byte's business and the "now" that must be adhered to.

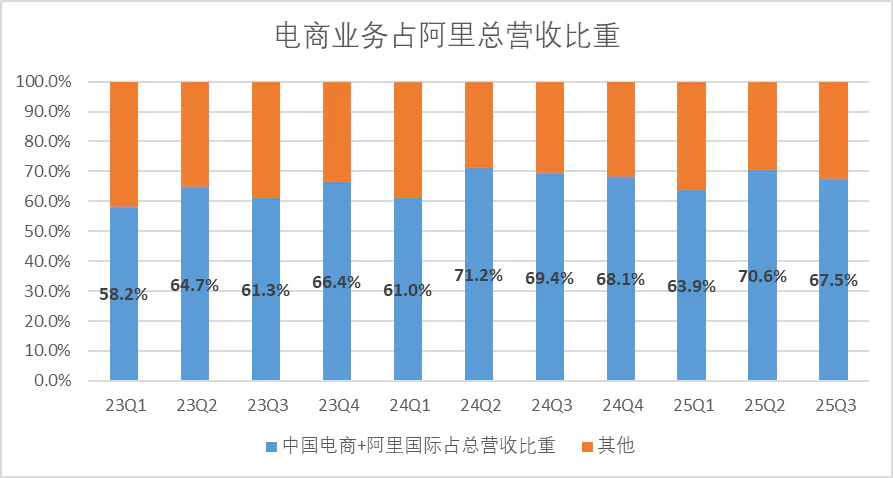

According to the data of fiscal year 2025, Taotian Group contributed about 45% of the group's revenue, and the proportion of revenue of the entire e-commerce sector (China E-commerce + Alibaba International) remained at 60%~70% all year round.

For Byte, the e-commerce business is the best way to efficiently monetize its huge traffic, which not only brings huge transaction volume, but also promotes Byte's transformation from a company dominated by advertising revenue to an "empire" with a more complex and robust business ecosystem.

Second, AI is the future that all giants are betting on.

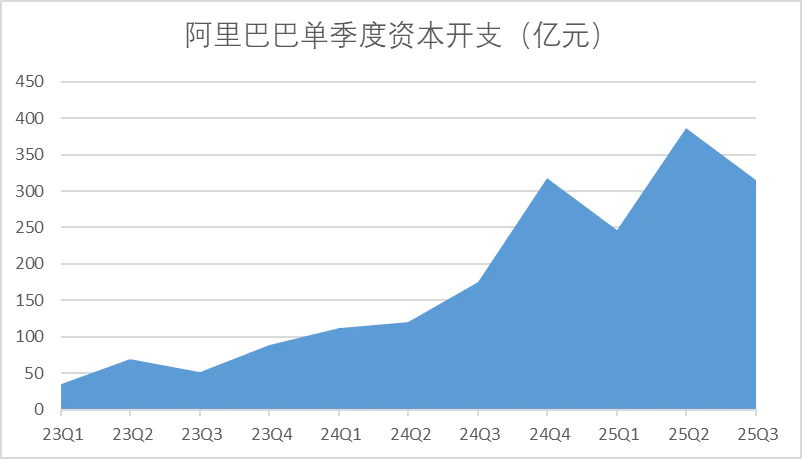

In February this year, Alibaba announced that it would invest 380 billion yuan in the next three years to build cloud and AI hardware infrastructure, becoming a full-stack AI technology company with AI computing power, AI cloud platform, AI models, open source ecology to AI applications. Facts have proved that Alibaba has done what it says: Alibaba's cumulative capital expenditure has exceeded 126 billion yuan in the past 12 months, and although capital expenditure has declined month-on-month in the third quarter, Alibaba's capital expenditure is actually not weak considering the background of limited AI computing power procurement and the obvious contraction of investment by other major players in the market (such as Tencent).

But Byte is not far behind. Zhejiang Securities once proposed in a research report that Byte's R&D investment is significantly ahead of its peers, and Byte may be analogous to OpenAI to the United States in China, and it acts more quickly. According to the data, its capital expenditure in 2024 has reached 80 billion yuan, the first among Chinese technology companies.

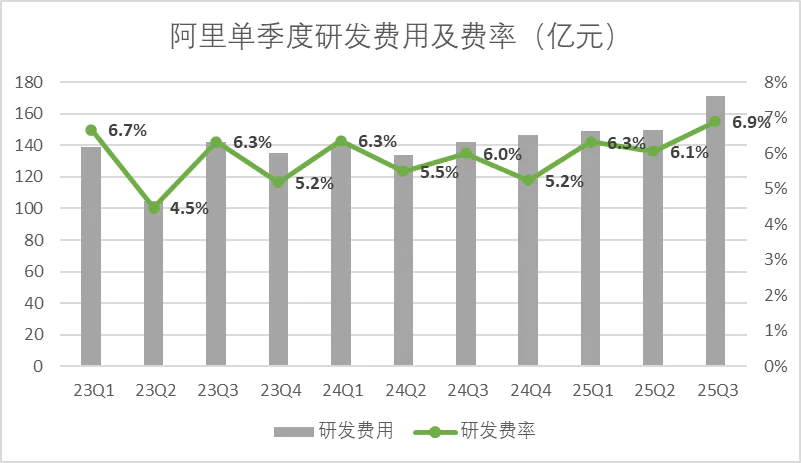

In the past few months, the competition between Alibaba and Byte has been overshadowed by the smoke of the takeaway war. With the current release of Alibaba's financial report, the outside world can get a glimpse of the changes in the Internet landscape. In the overall cost expenditure, in addition to the surge in marketing expenses brought about by takeaway, the cost of R&D investment is also rising, with a net increase of nearly 3 billion yuan year-on-year in the third quarter of this year alone.

The battle around the future seems to be more intense than imagined.

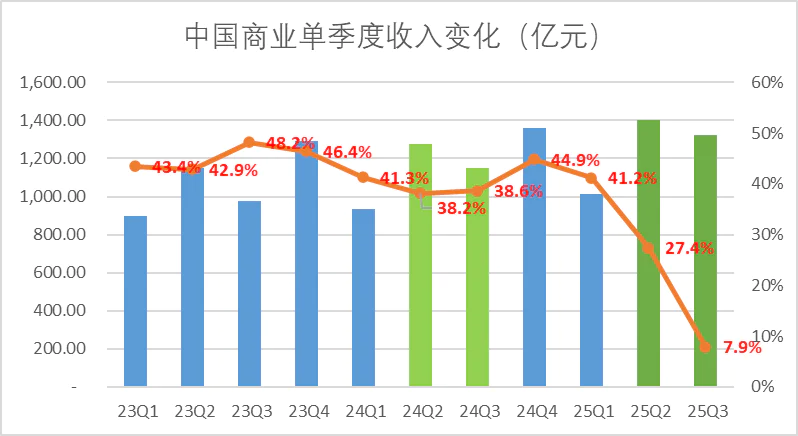

Second, takeaway has dragged Alibaba, and the advantages of e-commerce have been gradually eroded

To interpret e-commerce, we need to return to Alibaba's basic plate - China's business sector. One of the most obvious logics in its latest third-quarter earnings report is that the entire Chinese business is mired in instant retail, resulting in a cliff-like decline in single-quarter profit margins.

The group's non-GAAP profit in the third quarter was only 10.35 billion yuan, 6.5 billion yuan lower than the market's already relatively conservative expectations, and its core drag was the loss of the instant retail business far exceeding expectations. Judging from the single-quarter profit change alone, the net profit of China's commercial sector shrank by 33.8 billion yuan.

Assuming that its profit growth rate is basically the same as that of e-commerce revenue, then the actual loss of instant retail business may be as high as about 38 billion yuan, which is much higher than the scale reflected in the book figures. It is particularly worth noting that JD.com's single-quarter loss in the same period was only about 15 billion yuan - and Alibaba still invested so much when it already had Ele.me's infrastructure.

Alibaba's high-intensity investment has a very limited return:

According to the financial report, the growth rate of instant retail in the third quarter was about 60%, but the actual increase was only about 8.6 billion yuan, which is less than a fraction of the input cost.

Excluding the contribution of instant retail, the overall growth rate of China's e-commerce business is only 8%. In contrast, the average growth rate of China's commercial (excluding local life) revenue in the third to fourth quarters of last year was 11.5%, which shows that the driving effect of instant retail on e-commerce conversion is very weak.

Customer management (CMR) revenue growth in the third quarter was 10%, flat month-on-month. Considering that there was a technical service fee policy in September last year to drive the increase in CMR, it is indeed good on the surface that the growth rate can be maintained this year. However, in September last year, the technical service fee actually adopted the annual fee hedging method, which had a limited impact on CMR. The CMR of 24Q3 accounted for 71% of Taotian's total revenue, which was not much different from 24Q2.

(Take Rate)

More importantly, the policy dividend of technical service fees in the fourth quarter will no longer exist. The management also clearly lowered its expectations for CMR growth in the performance meeting. This means that the traffic growth brought about by instant retail is also very limited in improving the monetization efficiency (Take Rate) of traditional e-commerce.

Judging from this financial report, Alibaba's return on capital expenditure on instant retail is low - whether it is for the business itself or driven by e-commerce conversion, there is no effective positive feedback.

This may be the reason why Alibaba said in the earnings meeting that it would narrow its instant retail investment.

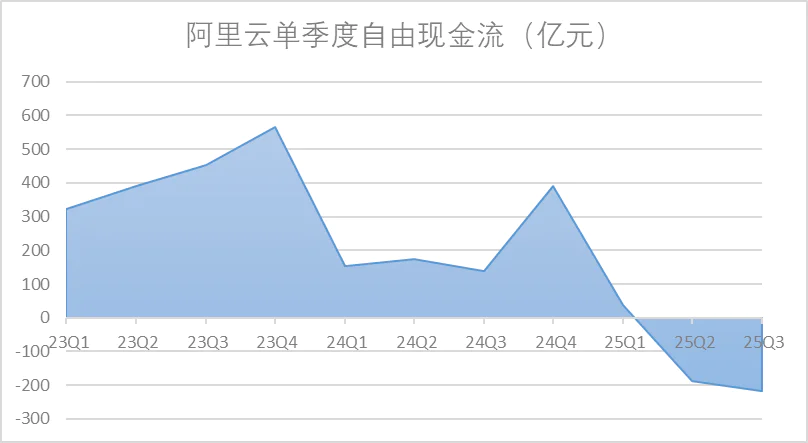

From takeaway wars to AI competitions, the essence of all business wars is a logistics battle. The winner of the logistics battle does not depend entirely on capital reserves, but on whether a positive cycle of "fighting to support war" can be built. At present, the AI business has initially shown signs of building healthy cash flow (although the road ahead is long, the cloud business is still the only visible incision to evaluate its AI strength in the current financial report); However, in the direction of pan-e-commerce, including instant retail, the situation is not optimistic.

At the same time, emerging e-commerce led by Byte performed well.

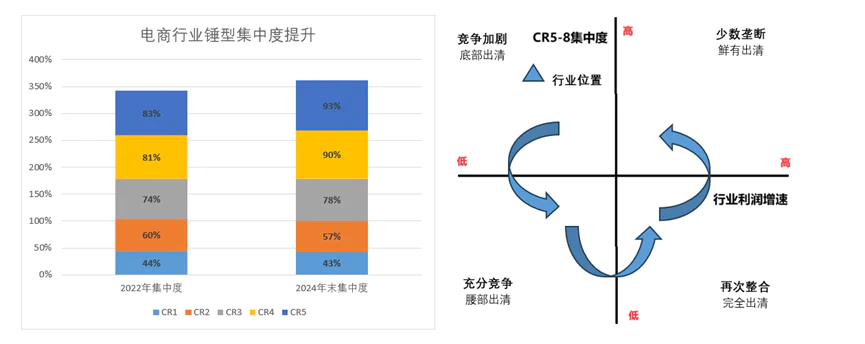

According to the "Late" report, Douyin's e-commerce GMV has exceeded 4 trillion yuan. According to Guosen Securities research, its growth mainly comes from the squeeze on the share of leading platforms such as Taotian and JD.com. The report also pointed out that a number of secondary market investors estimate that Taobao's payment GMV is about 6 trillion yuan. If both sides maintain their current growth rate, Taobao's leading position may be overtaken in the next few years.

According to research by Guosen Securities, the concentration of CR2 in domestic e-commerce in 2022 will be 60% and CR5 will be 84%; As of the beginning of this year, CR2 has dropped to 57%, and CR5 has soared to 93%, showing a "hammer" competition pattern with a concentrated head and a clear tail.

In a fully competitive environment, the e-commerce industry is gradually entering the clearing stage, and the head platforms have to increase investment to stabilize their position, and new players such as Xiaohongshu and Bilibili are also continuing to erode the original market share.

At this point, Byte and Xiaohongshu have the advantage of "cheap" traffic as content platforms, which has always been a headache for Ali. For a long time, Alibaba only consumed traffic, not produced traffic. To this end, Alibaba has invested in content platforms such as Weibo and Xiaohongshu to divert traffic to e-commerce. However, as e-commerce competition intensifies, Alibaba's traffic model operating costs continue to increase, as platforms such as Douyin will give priority to their own e-commerce business.

According to QM data, at present, Taobao's DAU is about 440 million, Pinduoduo's DAU is about 380 million, and Douyin is more than 800 million, and the latter has a huge advantage in terms of user usage time and opening frequency.

These are the dilemmas that Alibaba e-commerce has to face.

3. The AI competition between giants will intensify in 2026

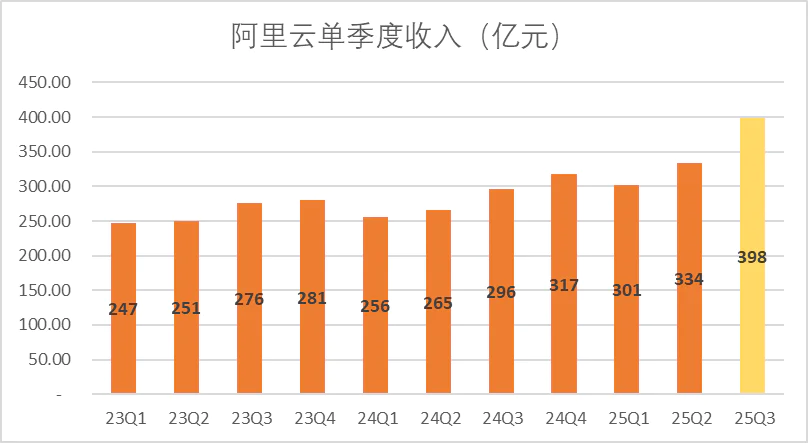

Of course, Alibaba's third-quarter report is not all bad news: Alibaba Cloud slightly exceeded market expectations in terms of revenue and profit. This performance also provides support for Alibaba to maintain relatively strong confidence in capital expenditure.

As one of the few businesses in the current market that can intuitively reflect the value of AI, the cloud business has been regarded as a key incision to observe the development of the company's AI capabilities. Alibaba Cloud has exceeded expectations in terms of performance and profit growth this time, which to some extent responds to the existing perception of the market: Alibaba is a leading Chinese AI target with the ability to handle the whole chain from computing power, traffic entrance to practical application.

Although Alibaba has a whole industry chain layout in AI: in terms of infrastructure, chips include Yitian and Xuantie, Lindorm at the data processing level, and Alibaba Cloud in computing power; In terms of models, the basic large model has a thousand questions and the application tools have a hundred refinements; At the application level, there are a number of cutting-edge apps such as Qianwen and Quark.

But in the most critical AI to C, Alibaba is not as good as Byte in terms of potential energy.

Taking Alibaba's recently promoted Qianwen App as an example, on November 24, Alibaba announced that its AI assistant Qianwen App has been in public beta for a week, and the number of downloads has exceeded 10 million, surpassing ChatGPT, Sora, and DeepSeek to become the fastest-growing AI application in history. However, the App Store free list shows that Doubao is still the number one AI application.

Considering only from the C-end import products, Byte also has the content and social ecological advantages that Alibaba lacks, and can be promoted at a lower cost. Douyin's content ecology around "Doubao" has been active for nearly a year, and if "Qianwen" wants to achieve the same volume, it needs to pay a higher price.

To be China's ChatGPT, Qianwen must first pass the byte level. But the problem is that with the speed of AI burning money, as strong as Alibaba also needs more ammunition support.

In this context, the cracks left by Alibaba's previous expansion are particularly tricky: if the e-commerce business cannot maintain its existing market leadership, how to ensure the sustainability of cash flow in multi-front operations? In fact, since entering the takeaway battlefield in the second quarter of this year, Alibaba's free cash flow in a single quarter has turned from positive to negative, and the net outflow has shown an expanding trend.

Betting on AI is something that Alibaba will inevitably do in 2026, but the intensity of competition it will face is bound to be much higher than the instant retail battle in 2025.

Compared with relatively narrow tracks such as local life, this competition is more difficult and the capital consumption is more intense. Judging from the current financial report, the pulling effect of instant retail on the basic market of e-commerce is indeed limited, and Alibaba's contraction front has been realistically necessary and urgent.

In every key battlefield such as e-commerce, AI, and cloud services, Alibaba is approaching the point of confrontation with Byte, which has the same strong capital strength. It is foreseeable that around the main axis of "e-commerce + AI", 2026 will usher in a "Battle of Tianwang Mountain".